Artificial Intelligence has become one of the largest infrastructure build-outs in modern history. Companies are investing hundreds of billions of dollars into GPUs, datacentres, networking equipment and power infrastructure to support increasingly capable AI models.

It can be difficult to understand where different companies fit into the ecosystem because everything is often grouped together under the label "AI". In reality, there are several distinct layers, each serving a different purpose.

Understanding these layers is essential for understanding where value is being created, where capital is being spent and where the risks lie.

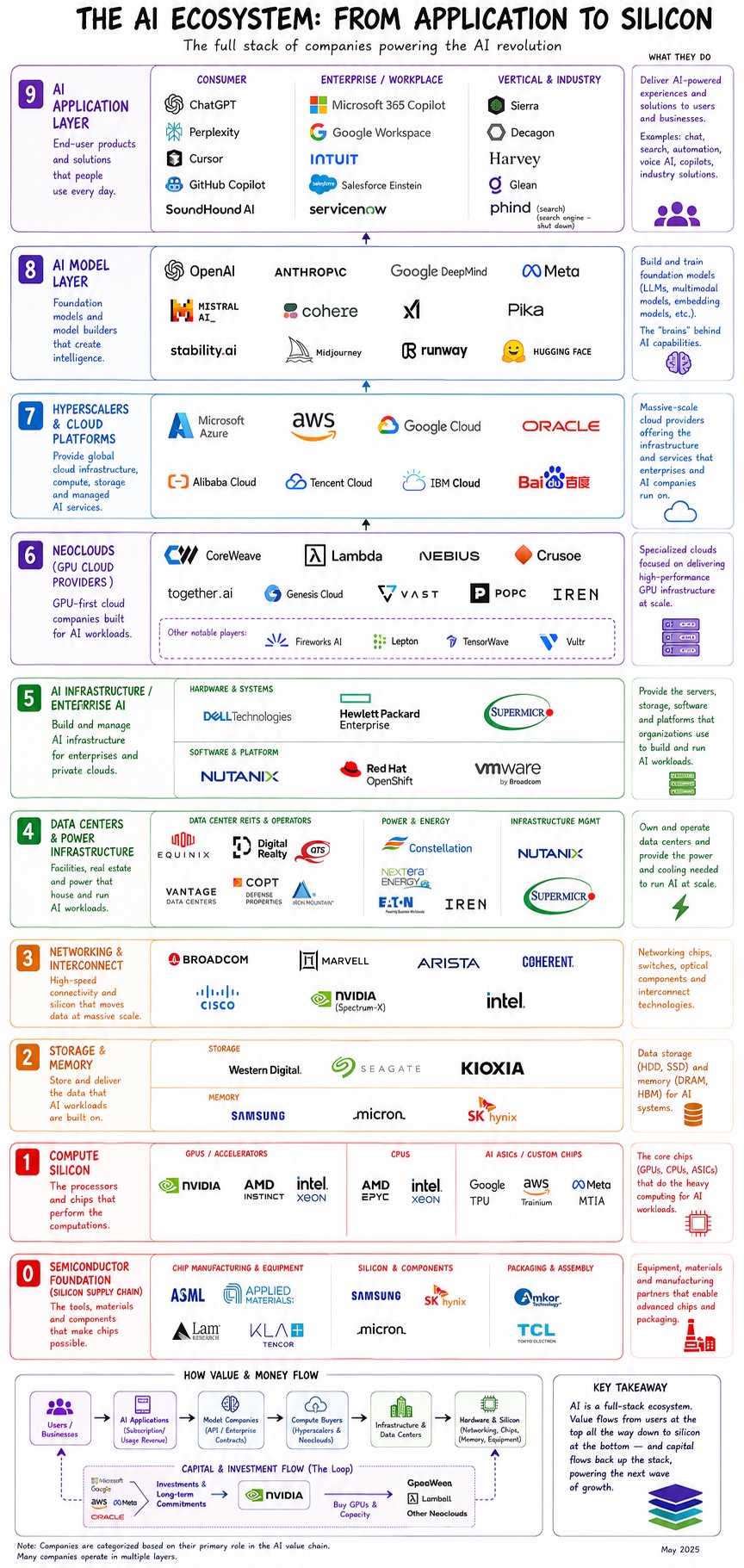

The AI Ecosystem

Application Layer

Most people interact only with the application layer. This is where end-user value is created.

Asking ChatGPT a question, using Cursor to write code, or using Perplexity to search the web are all examples of the application layer.

While some companies own both the application and the underlying model (such as OpenAI and Anthropic), the application remains the user-facing product.

Ultimately, every layer beneath the application layer is being built because investors and operators expect value to emerge here.

The key question is simple:

Do AI applications create enough value and return on investment to justify the enormous infrastructure being built beneath them?

AI Model Layer

The AI model layer is where the intelligence lives.

Model companies build and train foundation models and provide inference services that generate outputs in response to user requests.

This process requires enormous amounts of compute, data and capital.

Examples include:

- OpenAI (GPT)

- Anthropic (Claude)

- Google DeepMind (Gemini)

- Meta (Llama)

- Mistral

- Cohere

Model categories include:

- Large Language Models (LLMs)

- Image Models

- Video Models

- Speech Models

- Embedding Models

- Recommendation Models

- Robotics Models

- Scientific Models

Today, LLMs are the primary driver of AI infrastructure spending.

Hyperscaler Layer

The bridge between model companies and the infrastructure stack.

Examples:

- AWS

- Microsoft Azure

- Google Cloud

- Oracle Cloud Infrastructure

Hyperscalers provide:

- Compute

- Storage

- Networking

- Managed services

Historically these companies powered websites, SaaS applications and databases. AI workloads are significantly more demanding, requiring large numbers of GPUs and substantially greater infrastructure investment.

Neocloud Layer

Cloud providers optimized almost entirely for AI workloads.

Examples:

- CoreWeave

- Lambda

- Nebius

- Crusoe

Neoclouds emerged because traditional cloud providers could not supply enough AI compute quickly enough and because AI workloads differ significantly from traditional cloud workloads.

Unlike hyperscalers, neoclouds focus almost entirely on GPU infrastructure.

Neoclouds appear to carry some of the highest financial risk within the AI ecosystem. Many are funding rapid expansion through debt and equity while competing in a market whose long-term demand remains difficult to forecast.

Key risks include:

- Massive upfront capital expenditure

- Rapid hardware depreciation

- High debt levels

- Intense pricing pressure

AI Infrastructure Layer

Builds and operates AI computing systems.

Examples:

- Dell

- HPE

- Supermicro

- Nutanix

These companies provide:

- AI servers

- Storage systems

- Networking equipment

- Integrated AI infrastructure solutions

Datacentre Layer

Provides the physical facilities required to run AI infrastructure.

Examples:

- Equinix

- Digital Realty

- Applied Digital

- QTS

- Vantage

Datacentres provide:

- Buildings

- Power

- Cooling

- Physical security

- Connectivity

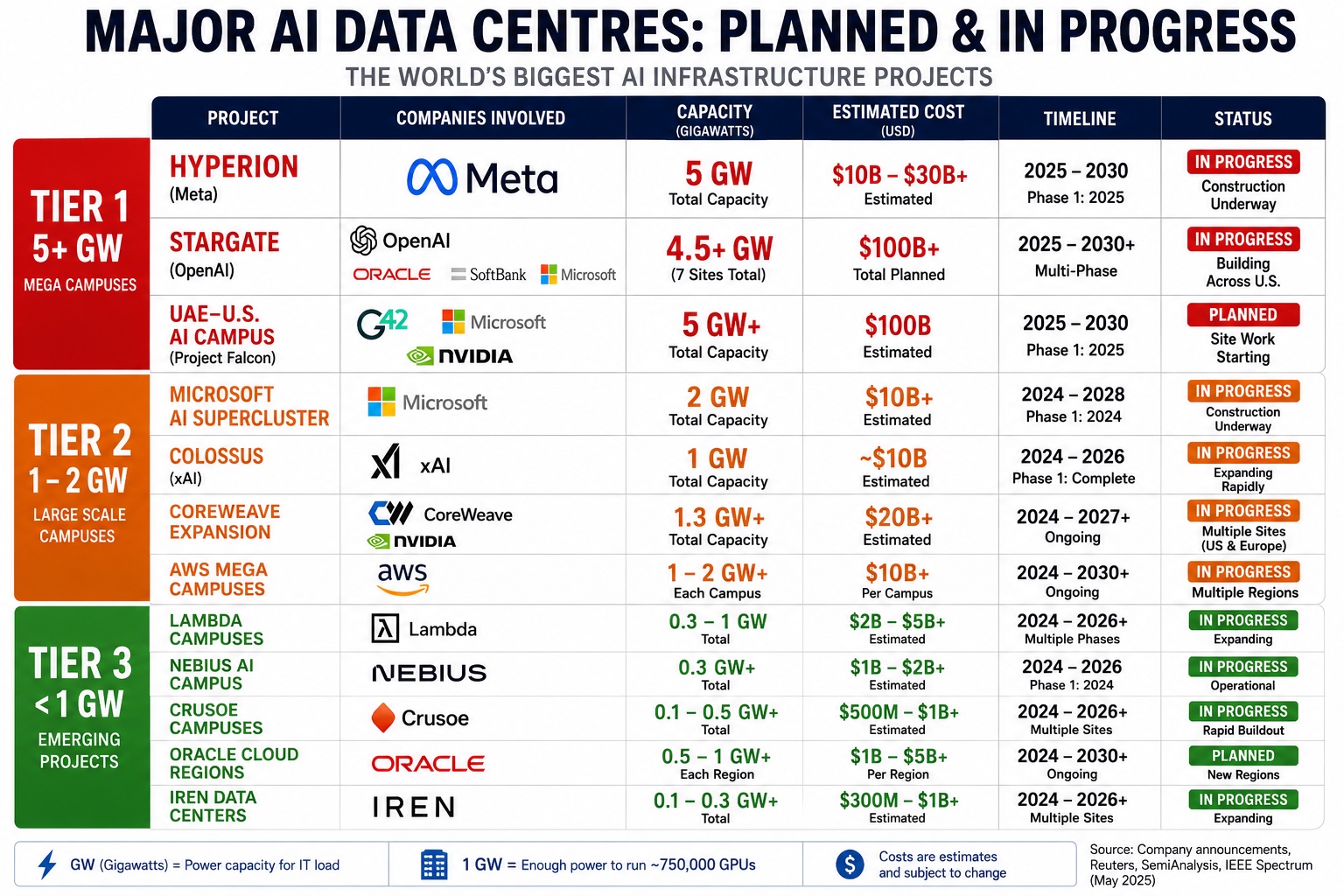

The AI industry is currently engaged in one of the largest infrastructure build-outs in modern technology history.

Hundreds of billions of dollars are being committed to GPUs, power infrastructure and datacentres before the long-term economics of AI have been fully proven.

The Physical Layer

The physical layer provides the hardware that powers every AI request.

Without this layer, models cannot be trained and applications cannot operate.

Networking

Moves data between GPUs, servers and datacentres.

Examples:

- Arista

- Broadcom

- Marvell

- Cisco

- HPE (Juniper)

Modern AI training requires tens of thousands of GPUs working together. Networking determines how efficiently those systems communicate.

Storage

Stores training data, model weights and user data.

Examples:

- Seagate

- Western Digital

- Pure Storage

Without storage there is no data available for training or inference.

Compute & Memory

Performs the calculations required to train and run AI models.

Examples:

- Nvidia

- AMD

- Intel

- SK Hynix

- Micron

- Samsung

- Google TPU

- Cerebras WSE

While Nvidia has become the face of AI demand, high-bandwidth memory supplied by companies such as SK Hynix, Micron and Samsung is equally critical to modern AI systems.

Google TPU (Tensor Processing Unit) and Cerebras WSE (Wafer-Scale Engine) are specially designed for the kind of operations done and to reduce netwokring bottlenecks between GPUs respectively.

Semiconductor Foundations

Design and manufacture the hardware powering the entire AI ecosystem.

Foundries

- TSMC

- Samsung Foundry

Semiconductor Equipment

- ASML

- Applied Materials

- Lam Research

- KLA

These companies sit at the very bottom of the stack but are foundational to everything built above them.

The Central Question

Every layer of the AI ecosystem ultimately depends on demand from the application layer.

Applications

↓

Models

↓

Create Demand

↓

Require Compute

↓

Justify Infrastructure

If applications create sufficient value, today’s infrastructure spending may prove justified.

If they do not, significant capital may have been allocated to infrastructure that fails to earn an adequate return.

Why AI Is Different From SaaS

Traditional SaaS businesses often enjoy extremely high margins.

Once software is built, serving an additional customer is relatively inexpensive. An email, CRM update or web request costs very little to process.

AI is different.

Every prompt, image generation request and agent workflow requires substantial computation.

Inference consumes:

- GPUs

- Memory

- Networking

- Electricity

And that is only the operational cost.

Model companies must also spend heavily on:

- Training new models

- Improving existing models

- Building infrastructure

- Acquiring compute capacity

This makes AI economics fundamentally different from traditional software economics.

Bringing It All Together

Applications

↓

Models

↓

Hyperscalers & Neoclouds

↓

Infrastructure & Datacentres

↓

Networking, Compute & Memory

↓

Semiconductor Foundations

Value flows downward from the application layer.

Capital flows upward from the physical layer.

The question facing investors is not whether AI will be important.

The question is whether the economic value ultimately created by AI applications will justify the unprecedented levels of infrastructure spending currently taking place beneath them.

Looking Ahead

The scale of investment currently underway is extraordinary, with hundreds of billions of dollars being committed to AI infrastructure worldwide.

Whether these investments ultimately generate attractive returns remains one of the most important questions facing the technology industry.

Future articles will examine:

- The financial performance of AI companies

- AI inference economics

- Profitability and margins

- Datacentre economics

- Risks associated with the current infrastructure build-out

- Potential winners and losers across the AI stack

![]()